How to Check CIBIL Score for Free in India (Step-by-Step Guide)

Your CIBIL score plays a major role in determining whether banks approve your credit card or loan applications. Before applying for any credit product, it is always wise to check your credit score first.

Many people assume checking their CIBIL score is complicated or expensive. In reality, several platforms allow individuals to check their credit score for free.

This guide explains how to check your CIBIL score in India step-by-step and what the score actually means.

What Is a CIBIL Score?

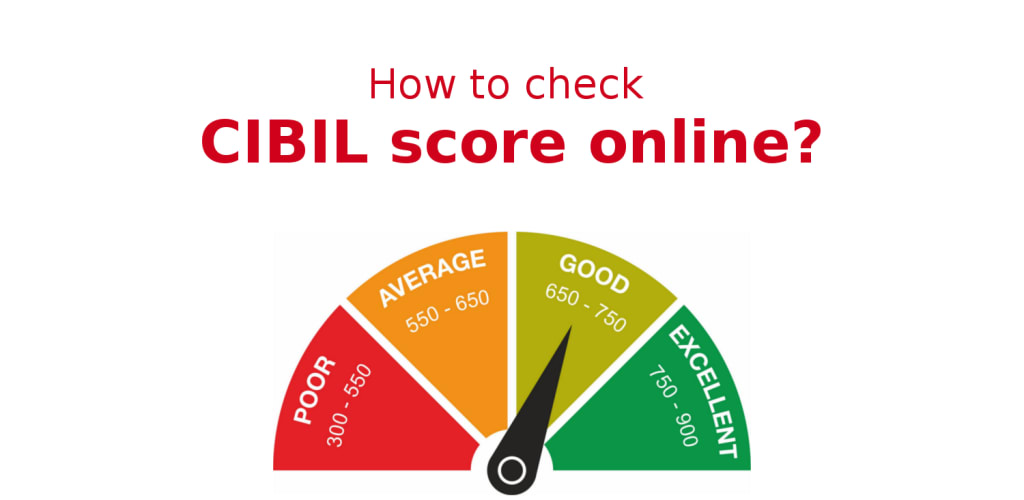

A CIBIL score is a three-digit number ranging from 300 to 900 that reflects your credit history and repayment behaviour.

The score is calculated based on your credit report maintained by major credit bureaus in India.

Banks and financial institutions review this score before approving credit cards, personal loans, and home loans.

What Is Considered a Good CIBIL Score?

- 750 – 900 : Excellent

- 700 – 749 : Good

- 650 – 699 : Average

- Below 650 : Risky for lenders

Generally, a score above 700 increases the chances of credit approval.

Why Checking Your CIBIL Score Is Important

Checking your credit score before applying for financial products helps you understand how lenders view your financial behaviour.

It allows you to:

- Identify errors in your credit report

- Understand your credit eligibility

- Improve your financial planning

- Avoid unnecessary credit rejections

If your score is lower than expected, you can work on improving it before applying for credit.

Your credit score also affects whether banks approve your card application. Learn how lenders evaluate applicants in our guide on credit card eligibility in India.

Does Checking Your CIBIL Score Reduce It?

No. When you check your own credit score, it is considered a soft enquiry and does not affect your score.

Only lender enquiries during loan or credit card applications are recorded as hard enquiries.

How to Check CIBIL Score for Free in India

Several platforms provide free credit score access. The process usually takes only a few minutes.

Step 1: Visit a Credit Score Platform

You can check your credit score through credit bureaus or financial platforms that partner with them.

Step 2: Create an Account

Enter basic details such as your name, mobile number, email address, and date of birth.

Step 3: Verify Your Identity

You may be asked to enter your PAN number and complete a mobile OTP verification.

Step 4: Access Your Credit Score

Once verification is complete, the platform will display your credit score along with key information from your credit report.

What Information Appears in a Credit Report

In addition to your credit score, the report typically includes:

- Active loan accounts

- Credit card limits and balances

- Repayment history

- Recent credit enquiries

This information helps lenders evaluate how responsibly you have handled credit in the past.

Many credit score problems occur due to avoidable financial habits. Understanding these issues can help prevent future problems. See our guide on credit card mistakes in India.

Common Reasons for a Low CIBIL Score

If your credit score is lower than expected, some common reasons may include:

- Missed or delayed EMI payments

- High credit card utilisation

- Too many credit applications

- Loan settlements or defaults

Even a few missed payments can significantly reduce your score.

If your application has already been declined due to a low score, you may find this helpful: credit card rejected due to low CIBIL score in India.

How Often Should You Check Your Credit Score?

Experts recommend checking your credit score at least two to three times per year. This helps ensure that your credit report remains accurate and up-to-date.

Regular monitoring also allows you to detect any fraudulent activity or reporting errors early.

How to Improve Your CIBIL Score

If your score is lower than expected, several steps can help improve it over time:

- Pay EMIs and credit card bills on time

- Keep credit utilisation below 30%

- Avoid frequent credit applications

- Maintain older credit accounts responsibly

Consistent financial discipline gradually improves your credit profile.

If your score is lower than expected, you can take steps to improve it. Read our detailed guide on how to improve CIBIL score in India to understand practical ways to increase your credit score.

Practical Tip: Check Your Score Before Applying for Credit

Many credit card and loan rejections occur simply because applicants apply without checking their credit profile first.

Reviewing your score beforehand allows you to understand whether your profile meets typical lender requirements.

You can also read our detailed guide on improving credit scores in India.

What Happens If You Never Check Your Credit Score?

Many people apply for credit cards or loans without ever reviewing their credit report. While this may seem harmless, it can sometimes lead to unexpected problems.

If there are mistakes in your credit report, lenders may reject your application even though your financial behaviour is responsible. For example, a loan account that has already been closed might still appear as active, or a payment might be reported as late due to a technical error.

Checking your credit score periodically helps you detect such issues early. Correcting these errors can improve your credit profile before you apply for any financial product.

Difference Between Credit Score and Credit Report

People often use the terms “credit score” and “credit report” interchangeably, but they are not the same thing.

Your credit score is a numerical summary of your credit behaviour. The credit report, on the other hand, contains detailed information about your financial history.

The report typically includes:

- Details of all your active and closed loan accounts

- Credit card limits and current balances

- Repayment history over the past several years

- Recent credit enquiries made by banks

Lenders study this detailed report before making a lending decision.

How Frequently Your Credit Score Gets Updated

Your credit score is not calculated only once. It changes over time as lenders report new information to credit bureaus.

When you repay a loan EMI on time, reduce credit card balances, or close a loan account, these updates are gradually reflected in your credit report. Similarly, missed payments or new loan enquiries may lower your score.

Because of these regular updates, checking your score periodically helps you stay aware of your financial position.

Simple Habits That Help Maintain a Healthy Credit Score

Maintaining a strong credit score does not require complicated strategies. A few simple habits can make a significant difference over time.

- Pay all EMIs and credit card bills before the due date

- Avoid using the entire credit limit on your cards

- Limit the number of new loan applications

- Review your credit report periodically for accuracy

These habits gradually build trust with lenders and improve your chances of credit approval in the future.

Monitoring Your Credit Score as a Financial Habit

Checking your credit score should be treated as a normal financial routine, similar to reviewing your bank balance or tracking monthly expenses.

When you stay informed about your credit profile, you can take corrective action early and avoid unpleasant surprises during important financial decisions such as applying for a home loan or credit card.

Regular monitoring ensures that your financial reputation remains strong and reliable.

Frequently Asked Questions

Can I check my CIBIL score for free?

Yes, several platforms allow individuals to check their CIBIL score for free once every year or through partner services.

How long does it take to check a credit score?

The process usually takes only a few minutes after completing identity verification.

What is the minimum CIBIL score required for a credit card?

Most banks prefer a score above 700, though entry-level cards may accept slightly lower scores depending on income and other factors.

Conclusion

Your CIBIL score is one of the most important indicators of your financial reliability. Checking it regularly helps you stay aware of your credit standing and avoid surprises when applying for loans or credit cards.

By monitoring your credit report and maintaining responsible financial habits, you can gradually build a strong credit profile and improve your eligibility for future financial products.