Personal Loan Rejected Due to Low Salary in India – What to Do

Getting a personal loan rejection due to low salary can be frustrating, especially when you have a stable job and regular income. Many applicants assume that loan approval depends only on employment status, but banks evaluate repayment capacity carefully before issuing unsecured loans.

Understanding why lenders reject applications due to income concerns can help you take the right steps before applying again.

Minimum Salary Requirement for Personal Loan in India

Most banks and NBFCs prefer applicants with a minimum monthly salary between ₹15,000 and ₹30,000 for entry-level personal loans. However, this requirement can vary depending on the lender, city of residence, and credit profile.

Premium loan products or higher loan amounts often require stronger income levels and longer employment stability.

Why Personal Loan Applications Get Rejected Due to Low Salary

Salary is used by lenders to estimate how comfortably you can repay EMIs without affecting daily expenses. Even if your income meets the basic eligibility threshold, rejection may still occur due to additional factors such as:

- Existing loan EMIs reducing repayment capacity

- High credit card outstanding balances

- Unstable employment history

- Recent loan enquiries

These risk indicators influence approval decisions along with income.

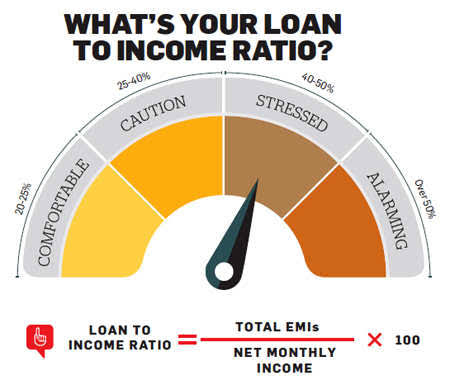

Understanding EMI to Income Ratio

Banks typically calculate an applicant’s EMI to income ratio before approving a loan. If a large portion of your salary is already committed towards existing EMIs, lenders may consider the risk of default higher.

Maintaining a manageable debt burden improves approval chances.

Does Credit Score Matter Even if Salary Is Low?

Yes. Credit score plays an important role in personal loan approval decisions.

Applicants with strong repayment history and disciplined credit usage may still qualify for smaller loan amounts even with modest income levels.

Even if salary is modest, a strong credit profile can improve approval chances. You can follow practical steps explained in our guide on how to improve CIBIL score in India.

Improving your credit score before applying can strengthen your loan eligibility.

What To Do After Personal Loan Rejection

1. Review Your Credit Report

Check whether late payments or incorrect entries are affecting your credit profile.

2. Reduce Existing Debt

Paying off small loans or reducing credit card balances can improve repayment capacity.

3. Consider Applying for Lower Loan Amount

Applying for a realistic loan amount aligned with your salary improves approval probability.

4. Apply Where You Have Salary Account

Banks may evaluate existing customers more favourably because income flow is visible.

Alternative Options if Salary Is Low

- Secured loans against fixed deposits

- Small consumer durable loans

- Add-on loan applications with co-applicant

These options help build repayment track record for future eligibility.

How Long Should You Wait Before Applying Again?

Financial advisors usually recommend waiting at least two to three months before submitting another loan application. This allows time to improve financial profile and reduces multiple enquiry impact.

If you have also faced credit card rejection due to credit score concerns, you may find this helpful: credit card rejected due to low CIBIL score in India.

Practical Insight: Matching Loan Size With Income

Many rejections occur because applicants apply for higher loan amounts than their salary supports. Choosing realistic loan size aligned with repayment capacity significantly improves approval chances.

How Lenders Assess Income Stability

Income level alone does not determine loan approval. Lenders also examine how stable your income has been over time. Frequent job changes, probation periods, or irregular salary credits may reduce confidence in repayment ability.

For example, an applicant earning ₹25,000 per month but working in the same organisation for two years may be considered lower risk compared to someone earning ₹30,000 but having changed jobs multiple times within a short period.

Providing consistent salary slips and bank statements helps strengthen your application.

Impact of Existing Credit Card Usage on Loan Approval

Credit card behaviour plays a significant role when banks evaluate personal loan applications. High credit card utilisation or delayed payments can signal financial pressure even if salary meets minimum requirements.

Lenders often review the percentage of credit limit being used. Regularly using more than 70–80% of available limit may reduce approval chances.

Reducing outstanding balances before applying can improve repayment capacity assessment.

Role of City and Employer Category

Loan eligibility criteria may vary depending on the city where you work. Applicants in metropolitan cities often face higher income thresholds because of increased living costs and lending risk models.

Similarly, employment with reputed organisations or government institutions may improve approval probability due to perceived job security.

Loan approval depends on several financial factors similar to credit card applications. These eligibility rules are explained in our article on credit card eligibility in India.

Importance of Maintaining Emergency Savings

Lenders prefer applicants who demonstrate financial discipline. Having an emergency fund shows that you can manage unexpected expenses without relying entirely on borrowed money.

Even saving a small portion of monthly salary consistently can create a positive financial profile over time.

Common Mistakes Applicants Make After Loan Rejection

One of the biggest mistakes is applying to multiple lenders immediately after rejection. Each new application generates a hard enquiry on your credit report, which may further reduce approval chances.

Another common issue is applying for the same loan amount without making any financial improvements. Instead, applicants should focus on reducing debt, improving credit behaviour, and waiting for profile updates.

Managing monthly expenses effectively can improve repayment ability. Creating a structured plan using a monthly budget in India helps reduce financial stress.

How Small Financial Improvements Increase Approval Chances

Loan approval decisions are often influenced by small but consistent financial improvements. Clearing overdue payments, reducing credit utilisation, and maintaining stable employment for a few months can significantly strengthen your application.

Applicants who take time to improve their profile before reapplying are more likely to receive favourable outcomes.

Before applying again, it is advisable to review your credit profile. You can follow this step-by-step guide on how to check CIBIL score for free in India.

Considering a Co-Applicant for Better Eligibility

In some cases, adding a co-applicant such as a spouse or parent with stable income can improve loan eligibility. Combined income increases repayment capacity and reduces perceived lending risk.

However, both applicants become responsible for repayment, so this option should be used carefully.

Long-Term Benefits of Responsible Borrowing

Building a strong repayment record through smaller loans or secured credit products can gradually improve eligibility for larger financial products in the future.

Responsible borrowing habits not only increase approval chances but also help secure better interest rates and higher loan limits over time.

Frequently Asked Questions

Can I get a personal loan with ₹15,000 salary?

Some lenders may approve small loan amounts depending on credit score and existing obligations.

Does personal loan rejection affect credit score?

The rejection itself does not reduce score, but multiple loan enquiries may impact it.

How can I improve loan eligibility?

Reducing debt, improving credit score, and maintaining stable employment can help.

Conclusion

A personal loan rejection due to low salary is not permanent. By improving financial discipline, choosing suitable loan amounts, and strengthening credit profile, applicants can increase their chances of approval in future applications.